Are Insurance Premiums Too High in the UK? What Mortgage Clients Need to Know

If you’re arranging a mortgage, you’ve probably been offered life insurance, critical illness cover, or income protection at the same time.

But a growing number of UK homeowners are starting to ask:

Are insurance premiums higher than they should be?

The reality is—insurance pricing isn’t always as straightforward as it seems. And understanding how it works could save you money over the long term.

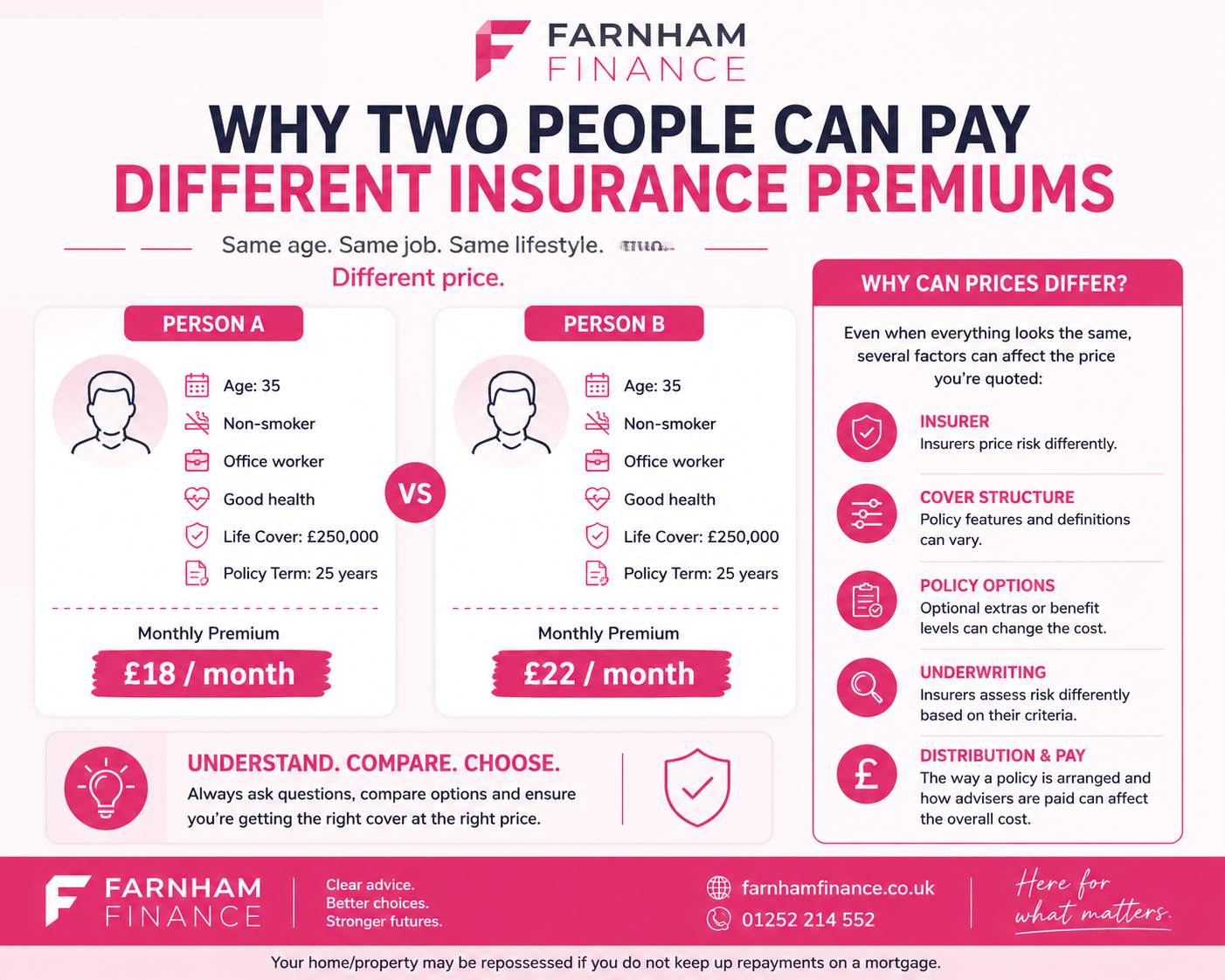

How Insurance Premiums Are Calculated in the UK

Insurance providers typically calculate premiums based on:

- Age

- Health and medical history

- Smoking status

- Occupation and lifestyle

- Type and level of cover

These are standard across the industry.

However, what many people don’t realise is that the route you take to arrange your policy can influence the price you pay.

Why the Same Insurance Policy Can Cost More

In some cases, two people with similar circumstances can end up paying different premiums for similar cover.

This often comes down to how the policy is structured and how advisers are paid.

Most insurance policies include commission from the insurer to the adviser. This is standard practice—but it can sometimes lead to:

- Higher long-term premiums

- Differences in pricing for similar products

- Less transparency around how costs are built

That doesn’t mean anything improper is happening—but it does highlight why understanding the cost structure matters.

Commission on Insurance: What You Should Know

Commission isn’t inherently a problem—it’s how most advisers are paid.

But it can create a potential conflict of interest if not clearly explained.

Under the Financial Conduct Authority’s Consumer Duty, firms must ensure customers receive fair value, meaning:

- The product is suitable

- The cost is reasonable

- The customer understands what they’re paying for

If pricing isn’t transparent, it becomes harder to assess whether you’re truly getting good value.

Are Some People Paying Too Much for Insurance?

Across the UK mortgage market, there’s increasing awareness that:

- Some customers may pay more than necessary for comparable cover

- Pricing differences aren’t always clearly explained

- Not all options are always presented

This doesn’t mean the industry is acting unlawfully—but it does reinforce the importance of clear, transparent advice.

How to Check If Your Insurance Premium Is Fair

If you’re arranging insurance alongside your mortgage, here are four key questions to ask:

1. Can you explain how you’re paid?

You should have a clear understanding of whether commission is included.

2. Are there alternative ways to structure the policy?

A good adviser should explain whether pricing could differ elsewhere.

3. How does this compare to the wider market?

This is where working with an experienced broker can make a real difference.

For example, at Farnham Finance, a full market comparison is used to ensure you’re not overpaying and are getting the right deal for your circumstances.

4. What is the total cost over time?

Monthly premiums matter—but so does the long-term cost.

Mortgage Protection Insurance: Cost vs Value

When it comes to protecting your mortgage, it’s not just about finding the cheapest policy.

It’s about:

- Getting the right level of cover

- Ensuring the price reflects the benefit

- Avoiding unnecessary costs built into the structure

If you’re currently reviewing your mortgage, it’s a good time to also review your insurance setup alongside your borrowing.

You can explore options for residential mortgage advice or review your deal when remortgaging or switching rates.

Choosing the Right Mortgage Broker for Insurance Advice

Not all brokers approach insurance in the same way.

At Farnham Finance, the focus is on:

- Clear, straightforward advice

- No broker fee for mortgage services

- Full market comparisons to ensure value

- Supporting both homeowners and landlords with tailored solutions

This approach is designed to help clients make informed decisions—not just quick ones.

Our Approach: Transparent Insurance Advice

When arranging insurance, the goal should always be clarity.

That means understanding:

- What you’re paying

- What you’re covered for

- How your adviser is remunerated

If you’re unsure about your current setup—or want a second opinion—it’s worth having a conversation.

You can request a call with a mortgage adviser to review your options and ensure everything is structured in your best interests.

Final Thoughts: Are Insurance Premiums Too High?

Insurance premiums in the UK aren’t fixed in the way many people assume.

While most advisers act in their clients’ best interests, pricing structures can vary—and that can affect what you pay.

The key takeaway?

Transparency matters.

When you understand how your policy is structured, you’re in a much stronger position to ensure you’re getting:

- The right cover

- At the right price

- With clear, fair advice

Need Help Reviewing Your Insurance?

If you’d like a clear, no-pressure review of your mortgage and insurance options, speak to Farnham Finance today.

You’ll get straightforward advice, full transparency, and a focus on long-term value—not just monthly cost.

Are insurance premiums fixed in the UK?

No. Insurance premiums can vary depending on your age, health, smoking status, occupation, lifestyle, cover level, insurer and how the policy is arranged.

Can a mortgage broker affect the cost of insurance?

In some cases, yes. The way a policy is arranged and how adviser remuneration works can influence the overall cost, so it is important to understand the structure clearly.

Is commission on insurance a bad thing?

No. Commission is common in the insurance industry. The key issue is whether it is explained clearly and whether the customer receives fair value.

How do I know if I am paying too much for insurance?

Ask how the premium was calculated, whether commission is included, whether alternatives were considered, and what the total cost will be over the full policy term.

Should I review insurance when remortgaging?

Yes. Remortgaging is a good time to review your protection needs, especially if your loan amount, term, income, family circumstances or monthly budget have changed.

| Question | Ask Your Adviser |

|---|---|

| How are you paid? | Ask whether commission is included |

| Why this insurer? | Ask how alternatives were assessed |

| What’s the total cost? | Look beyond monthly premiums |

| What am I covered for? | Understand exclusions and limitations |

Written by Robert Lewis-Crosby, Mortgage Adviser at Farnham Finance. Rob has over 10 years’ experience helping homeowners, landlords and property investors arrange mortgage finance across the UK.

Your home/property may be repossessed if you do not keep up repayments on a mortgage.