How Solicitor Referral Fees Work in Property Transactions

Understanding Recommendations, Transparency and Consumer Choice

When arranging a mortgage, remortgage or buy to let mortgage, you may be offered a recommendation for a solicitor or conveyancer.

For many borrowers, this feels like a natural part of the process. After all, if your mortgage broker recommends a solicitor, it is easy to assume they have been selected purely because they provide excellent service.

In reality, solicitor recommendations can arise for a variety of reasons. Sometimes it is because firms have worked successfully together for many years. Sometimes it is because the solicitor specialises in a particular type of transaction. In other cases, a referral fee arrangement may exist.

Referral fees are a legitimate and common part of the UK property industry. However, understanding how they work can help consumers make more informed decisions when choosing a solicitor.

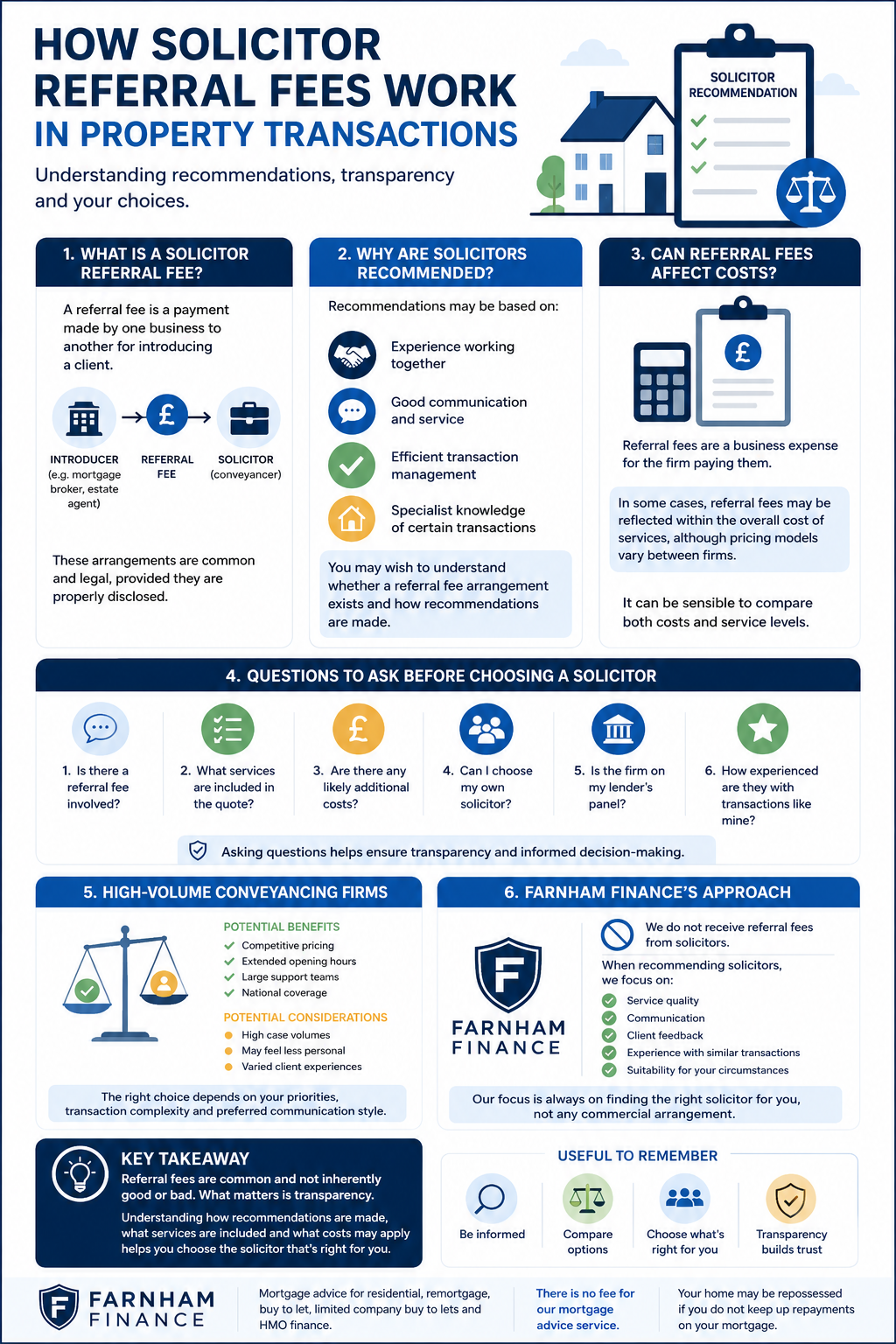

What Is a Solicitor Referral Fee?

A solicitor referral fee is a payment made by one business to another for introducing a client.

For example:

- An estate agent may recommend a conveyancing firm.

- A mortgage broker may recommend a solicitor.

- A financial adviser may recommend a conveyancer.

If the client proceeds with that firm, the introducing business may receive a referral fee.

These arrangements are permitted and widely used throughout the property sector, provided they are disclosed appropriately and comply with applicable regulations.

Why Are Solicitors Recommended?

Recommendations are often made for perfectly legitimate reasons.

A mortgage broker may recommend a solicitor because:

- They have experience dealing with mortgage lenders.

- They communicate well with clients.

- They regularly complete transactions efficiently.

- They understand specialist areas such as buy to let, limited company borrowing or HMOs.

However, consumers may wish to understand whether a referral arrangement exists and how recommendations are made.

Transparency allows borrowers to decide whether they are comfortable proceeding with a recommended firm or whether they would prefer to source their own solicitor independently.

Can Referral Fees Affect Costs?

Referral fees are a business expense for the firm paying them.

In some cases, referral fees may be reflected within the overall cost structure of a service, although pricing models vary between firms.

For this reason, it can be sensible to compare:

- Quoted legal fees

- Disbursements

- Service levels

- Communication standards

- Reviews and recommendations

The cheapest option is not always the best option, and the most expensive option is not always the best value.

What Questions Should You Ask?

If a solicitor is recommended to you, consider asking:

1. Is there a referral fee involved?

There is nothing wrong with asking this question.

A transparent business should be happy to explain any commercial arrangements.

2. What services are included?

A low headline fee can sometimes exclude additional work that may become chargeable later.

3. Are there any likely additional costs?

Ask about:

- Leasehold supplements

- Trust work

- Gifted deposits

- Limited company transactions

- Independent Legal Advice (ILA)

- Transfer of equity work

4. Can I choose my own solicitor?

In most mortgage transactions, the answer is yes.

You are generally free to choose whichever solicitor you prefer, subject to lender panel requirements.

High-Volume Conveyancing Firms

Some conveyancing firms operate large-scale, high-volume models.

This can offer benefits including:

- Competitive pricing

- Extended opening hours

- Large support teams

- National coverage

However, some clients may prefer a more personalised service with a dedicated point of contact.

There is no universally correct approach.

The right choice depends on your priorities, transaction complexity and preferred communication style.

Why Transparency Matters

The most important issue is not whether referral fees exist.

The most important issue is whether clients understand:

- How recommendations are made

- Whether referral fees are involved

- What services are included

- What alternatives are available

When consumers have clear information, they can make informed decisions based on value, service and suitability.

Farnham Finance’s Approach

At Farnham Finance, we do not receive referral fees from solicitors.

Instead, when clients ask for recommendations, we focus on:

- Service quality

- Communication

- Client feedback

- Experience with similar transactions

- Suitability for the client’s circumstances

This approach allows us to focus entirely on finding a solicitor who is appropriate for the transaction rather than any commercial arrangement.

Questions to Ask Before Instructing Any Solicitor

Before proceeding, consider asking:

✓ What is included in the fee?

✓ Are there likely to be any additional charges?

✓ Will I have a dedicated contact?

✓ How will updates be provided?

✓ Is the firm on my lender’s panel?

✓ Is there a referral arrangement involved?

✓ How experienced are they with transactions similar to mine?

Final Thoughts

Solicitor referral fees are a common and legitimate part of the UK property market.

The key issue is transparency.

Understanding how recommendations are made, what services are included and what costs may apply can help borrowers make informed decisions and choose the solicitor that best meets their needs.

Whether you use a recommended solicitor or select your own, taking the time to ask questions and compare options can help ensure a smoother property transaction.

Farnham Finance provides mortgage advice for residential mortgages, remortgages, buy to let mortgages, limited company buy to lets and HMO finance.

There is no fee for our mortgage advice service.

Your home may be repossessed if you do not keep up repayments on your mortgage.